Summarize Content With:

Banks have never invested more in technology and yet customers are still walking away after a single nasty phone call. Here is the reality most banking leaders do not want to admit:

- The financial sector leads nearly every industry in digital transformation spending from mobile apps to AI-powered fraud detection but the telephone front desk is often the last thing modernized.

- Automation is being deployed for the wrong reasons. Most front desk automation is built to reduce costs and deflect calls, not to actually help customers and customers feel the difference immediately.

- The gap between digital investment and telephone experience is widening. Banks build beautiful mobile apps but leave customers navigating a fifteen-year-old IVR maze the moment they call for help.

- The “first call failure” problem is born at this exact gap. Customers contact us during financial worry, but if the interaction proves poor, detached, or incomplete, confidence erodes immediately during that first contact.

- This is not a technology problem. It is a strategy problem. The tools exist to fix this. The question is whether banks are willing to prioritize the front desk experience the same way they prioritize their app store ratings.

This blog examines why first call failure happens, what it truly costs, and how deploying the right AI receptionist in the banking front desk or AI Receptionist for financial advisors can close the gap between automation investment and actual customer retention.

What Is the “First Call Failure” Problem?

First Call Resolution (FCR) is the metric that measures whether a customer’s issue is fully resolved on their first contact, no callback, no repeat visit, no escalation needed. In banking, FCR is not just an operational benchmark; it is a loyalty indicator.

When a customer’s first call fails when they are transferred three times, placed on hold for ten minutes, or ended up talking to an automated system that cannot understand them several things happen simultaneously:

- Their confidence in the bank drops sharply.

- Their emotional state shifts from transactional to adversarial.

- They begin mentally exploring alternatives.

The critical insight here is that first call failure is not always caused by agent incompetence. More often, it is caused by what happens before a human agent ever picks up the phone — the front desk experience itself.

“Customers don’t remember the department that solved their problem. They remember the experience of trying to reach someone who could.”

McKinsey & Company, State of Customer Care 2024

Why Banking Automation Alone Isn’t Enough to Retain Customers

Here is the uncomfortable truth: most banks automate for cost reduction, not for customer experience improvement. These two goals are not always aligned and in telephone front desk operations, they are frequently at odds.

The automation deployed at most banking front desks is built around deflection: get the customer to serve themselves or hang up before they reach a human agent. This deflection-first model works for cost metrics. It fails for customer metrics.

Consider the data. A survey found that 60% of customers abandon support requests if they wait too long. In banking, where the average caller is already stressed about money, patience thresholds are even shorter. Nearly half of the customers who exit a bank do so within the first 90 days of account opening the exact window when front desk interactions are most frequent and most formative.

And the stakes of losing them are enormous. The Qualtrics Banking Report found that customers who are sure they’re leaving their bank ranked “poor service” as the number one reason they’re leaving, and 56% of those who left say the bank could have changed their mind.

Banks are not just losing customers. They are losing customers who wanted to stay. But the AI call assistant is the real game-changer.

The Real Cost of a Failed First Call in Banking

Let us move beyond the abstract and put real numbers to this problem.

Banks offering callback options during high call volumes report a 17% drop in churn. This seemingly small UX decision offering a callback instead of forcing a hold correlates directly with retention. That is the power of front desk design.

One in five consumers worldwide, and one in four aged 18–43, switched providers in the past year due to poor communications. In banking, where switching a primary account has historically been considered a major friction event, this shift signals that the effort-to-leave is dropping rapidly, especially for younger customers.

The revenue implication is compounding. Customer lifetime value in banking accounting for deposits, loans, investment products, and referrals often exceeds $10,000–$30,000 per customer. A failed first call that leads to churn is not a $0 cost. It is a five-figure loss, multiplied across every customer who leaves silently without complaining.

“The most dangerous customer is not the one who complains loudly. It’s the one who says nothing and opens an account somewhere else next week.”

Forrester Research, Customer Loyalty in Banking 2025

Chart Insight First Call Failure Impact on Customer Lifetime Value:

Based on industry benchmarks:

- Average banking customer lifetime value: $15,000–$25,000

- Percentage of churners citing poor first contact experience: ~56%

- Percentage of churned customers who could have been retained: ~56%

- Estimated revenue at risk per 1,000 churned customers: $8.4M–$14M

(Source: Qualtrics Banking Report; McKinsey Customer LTV benchmarks)

How Traditional IVR Systems Make Things Worse

Interactive Voice Response (IVR) systems were revolutionary when they were introduced in the 1980s. They are not revolutionary now. Yet the majority of banking front desks still use IVR as their first line of customer interaction.

The problem with IVR in 2025 is not technological, it is philosophical. IVR was designed to route calls, not to resolve them. It maps customer needs onto a rigid menu tree that was built around what the bank wants to talk about, not what the customer actually called for.

Modern customers call a bank about a pending charge they do not recognize. IVR offers them options for account balance, loan applications, and branch hours. The mismatch is not just inconvenient, it is trust-eroding.

About 58% of customers abandon chat sessions when they realize a bot can’t resolve their issue. The same psychology applies to phone interactions. The moment a customer senses that the system cannot help them, they either escalate (increasing agent load) or abandon entirely (increasing churn risk).

Chatbots have helped reduce inbound call volumes by 42% in 2025, cutting down staffing needs but only when they are deployed correctly as front-end resolution tools, not call deflection tools.

The distinction matters enormously. Deflection says: “We don’t want to talk to you.” The resolution says: “We are going to help you right now.”

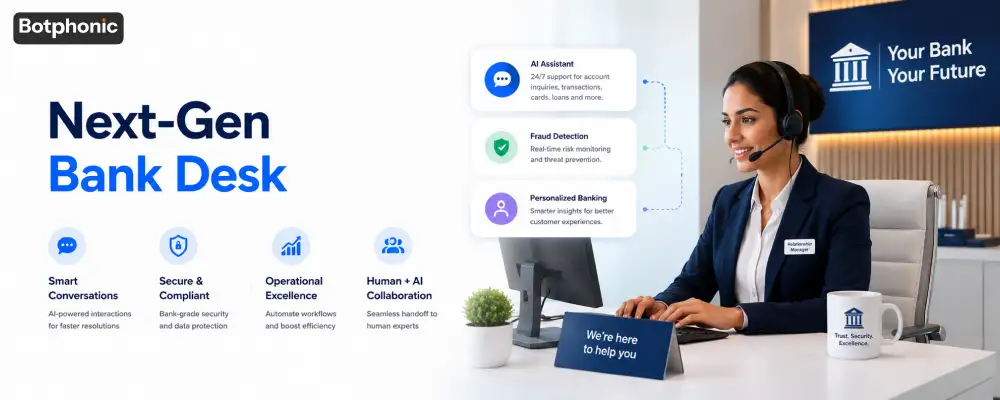

What an AI Receptionist in Banking Front Desk Actually Does Differently

An AI receptionist for banking is not a smarter IVR. It is a fundamentally different category of technology.

Where IVR routes, an AI receptionist understands. Where IVR deflects, an AI receptionist resolves or prepares a warm handoff to the human who can. The difference is felt by the customer in the first ten seconds of the call.

Here is what a properly deployed AI receptionist does at the front desk of a bank:

Instant, human-like answer

No hold music. No, “your call is very important to us.” The call is answered in under three seconds, in a natural voice that identifies the bank and opens the conversation.

Intent recognition, not menu navigation

Using natural language processing, the AI understands what the customer says in their own words “I got a text about a suspicious transaction” and routes or resolves accordingly, without forcing them through a decision tree.

Sentiment analysis

Modern AI receptionists can sense the tone of the client and adjust replies accordingly, providing empathetic replies that sound just like human responses. A customer who is distressed about a potential fraud event receives a different conversational tone than one asking about branch hours.

CRM integration

AI receptionists in banking and finance must integrate with CRM systems that update client information automatically, providing access to client history when needed. When a customer calls, the AI already knows their account status, last interaction, and open service tickets enabling personalized service from the first word.

Compliance-first design

AI receptionists built for banking operate within regulatory frameworks, flagging interactions that require human verification or recorded consent before proceeding.

The AI for financial service resolves 73% of calls without requiring a transfer or callback meaning nearly three-quarters of your incoming call volume is handled at the front desk without human intervention, and handled well enough that customers do not need to call back.

“The goal of AI at the front desk is not to replace human bankers. It is to make sure no customer ever experiences a dead end.”

Key Metrics: AI Receptionist vs. Traditional Front Desk

| Metric | Traditional IVR / Human Front Desk | AI Receptionist (Banking) | Source |

| Average call answer time | 45–90 seconds | Under 3 seconds | Juniper Research, 2025 |

| First Call Resolution Rate | 55–65% | 73–74% | CoinLaw Banking Stats, 2025 |

| Call abandonment rate | 15–25% | Under 5% | Sprinklr Call Center Report, 2025 |

| Operating cost per call | $6–$12 | $0.50–$2.00 | McKinsey AI in Operations, 2025 |

| 24/7 availability | Rarely | Always | Industry Standard |

| Sentiment detection | None | Real-time | Botphonic AI Banking, 2025 |

| Post-call churn risk reduction | Baseline | Up to 17% drop in churn | CoinLaw Retention Stats, 2026 |

(Sources: Banking Chatbot Adoption Statistics 2026: Usage, Efficiency & Security

Important Call Center Statistics to Know [2025]

40+ AI Receptionist Statistics You Need to Know (2026))

Common Implementation Mistakes Banks Make

Even banks that invest in AI receptionist technology often underdeliver on results. The technology is not the bottleneck implementation strategy is. The most common mistakes fall into predictable patterns:

Deploying AI as a gatekeeper, not a greeter. Some banks configure their AI receptionist to qualify customers out rather than in asking for account numbers, PINs, and security answers before offering any help. This creates the same deflection-first feeling that makes IVR frustrating. The AI should greet warmly, identify intent quickly, and route or resolve not interrogate.

No warm transfer protocol. When an AI phone call software for banks & fin-tech hands a call to a human agent, it should pass along a full context summary caller identity, stated issue, sentiment score, and CRM notes. Banks that treat the AI-to-human transfer as a fresh start eliminate the entire efficiency gain. The customer has to repeat themselves, frustration spikes, and the first call still fails.

Ignoring after-hours volume. A 27% average increase in booked appointments within the first 90 days of AI receptionist deployment comes primarily from capturing after-hours calls and reducing abandoned calls during busy periods. Banks that deploy AI only during business hours leave significant value on the table.

Failing to train the AI on real banking language. A generic AI receptionist that does not understand terms like “wire transfer cutoff,” “Reg D violation,” or “stop payment” will fail in the first week of deployment. Training on bank-specific vocabulary, product names, and workflows is non-negotiable.

Not measuring First Call Resolution separately from call deflection. These are different metrics with different implications. A deflected call is not a resolved call and conflating them hides the true performance of your front desk.

PRO TIP

PRO TIP

The Right Architecture: Hybrid AI + Human Model

The “First Call Failure” problem is not solved by AI alone. It is solved by the right combination of AI and human capability, deployed in the right sequence.

AI and human collaboration improves customer satisfaction scores by up to 20% compared to AI-only setups. The optimal front desk model works like this:

The AI receptionist handles the first point of contact 100% of incoming calls, 24/7. It resolves what it can (balance inquiries, appointment scheduling, general product information, fraud alert acknowledgment). For anything requiring judgment, empathy, or authorization, it performs a warm transfer passing the full context to a human agent who can pick up the conversation mid-stream, not from zero.

This architecture means human agents spend their time on genuinely high-value interactions, not on telling customers what their balance is or reading branch hours from a script. Their cognitive load drops. Their per-call resolution quality rises. And the customer experiences a seamless journey from automated front desk to expert human without ever feeling like they fell through a crack.

How to Evaluate an AI Receptionist for Your Bank

Not every AI answering service is built for the compliance, security, and integration requirements of a financial institution. Use this table as your evaluation checklist.

| Evaluation Criteria | What to Look For | Red Flag |

| Natural language understanding | Understands banking terminology without programming every phrase | Requires rigid keyword matching |

| CRM / Core banking integration | Native or API integration with your existing systems | Requires manual data entry post-call |

| Compliance features | Supports call recording consent, PCI-DSS data handling | No mention of regulatory framework |

| Sentiment analysis | Real-time emotional cue detection with tone adjustment | Binary happy/unhappy detection only |

| Warm transfer capability | Passes full context summary to human agents | Hard transfer only (customer repeats issue) |

| After-hours handling | Full resolution capability, not just voicemail | Routes to voicemail after hours |

| Multilingual support | Handles primary community languages automatically | English-only |

| Analytics dashboard | FCR rate, sentiment trends, call resolution breakdown | Only call volume and duration metrics |

| Customization | Brand-aligned voice, tone, and greeting | One-size-fits-all voice |

| Security | Encrypted call data, SOC 2 / ISO 27001 compliant | Vague security claims |

(Related reading: AI Receptionist Implementation Step-by-Step Botphonic)

Every day your banking front desk runs on outdated IVR or understaffed human lines, you are handing customers to competitors who answer instantly.

Botphonic AI is purpose-built for banks and financial institutions with sentiment analysis, CRM integration, compliance-first design, warm transfer protocols, and 24/7 coverage in multiple languages.

Request a Free Demo