Summarize Content With:

What You’ll Learn in This Blog

- Why generic AI chatbots fail banking compliance requirements

- What makes an AI receptionist truly financial-grade

- The compliance, security, and integration standards banks should evaluate

- How real banking AI deployments work in production

- Which platforms are actually built for regulated financial environments

- When AI voice automation is worth deploying, and when it isn’t

An AI receptionist for banking is an automated voice or chat system that handles inbound customer calls without a human agent. It is built for financial institutions, banks, credit unions, and lenders, that must balance call volume with strict regulatory requirements. Getting this wrong exposes institutions to fraud liability, compliance violations, and customer attrition.

What Is an AI Receptionist for Banking, and Why Does It Differ From a Standard Chatbot?

An AI receptionist for banking is not a general-purpose chatbot with a disclaimer attached. It is a purpose-built system operating inside fixed, compliance-approved workflows. Here’s what that means for your institution.

A standard customer service bot answers questions from a probabilistic language model. It generates responses. A financial-grade automated receptionist retrieves responses from a pre-approved script library and routes everything else. That distinction is the difference between regulatory exposure and defensible deployment.

Why open-ended LLMs cannot handle banking interactions

Large language models synthesize answers. That is their core capability, and their core liability in financial services.

Ask a general LLM about a customer’s balance, and it may attempt to generate a plausible-sounding number. Ask it about a loan rate, and it may confabulate terms your institution never offered. The Consumer Financial Protection Bureau has issued guidance warning that AI-generated financial misinformation exposes institutions to UDAAP liability.

Source: CFPB Guidance on Chatbots in Banking

Deterministic pipelines eliminate this risk. The AI retrieves; it does not generate.

Why IVR menus alone are not the answer either

Legacy interactive voice response systems do not solve the problem, they aggravate it. Nested IVR menus drive an immediate 20–30% drop in customer satisfaction scores during high-stress financial events (Forrester Research). Customers calling during a fraud alert or missed payment do not want to press 4 for more options.

The correct architecture sits between those two failure points: structured enough to enforce compliance, conversational enough to reduce abandonment. That is where a regulated AI call assistant becomes operationally valuable for banks and lenders.

Why Are So Many Banking AI Deployments Failing Compliance Audits?

Most banking AI deployments fail compliance audits because vendors prioritize demo performance over regulatory architecture. Here’s what that means for procurement teams.

Four failure patterns appear repeatedly in financial services AI deployments. Understanding them before issuing an RFP saves significant remediation costs.

Failure Point 1: Weak authentication protocols

Knowledge-based authentication, mother’s maiden name, last four digits, childhood pet, is no longer a defensible security layer. Voice cloning technology has made social engineering via synthetic audio a viable attack vector.

Financial-grade platforms must support multi-factor authentication via out-of-band PIN delivery or voice biometrics. Platforms that rely entirely on static security questions should be disqualified during vendor review.

Failure Point 2: The hallucination liability gap

Any platform that uses an open-ended LLM to respond to authenticated account inquiries creates direct regulatory exposure.

SOC 2 Type II certification tells you about data handling. It says nothing about whether the AI is generating account disclosures your compliance team never approved. Require vendors to demonstrate deterministic response pipelines, not just show you a compliance badge. That is why regulated AI customer service platforms avoid open-ended financial response generation.

Failure Point 3: Missing core banking API integrations

A voice AI that cannot write to your core banking system is an expensive FAQ page. For meaningful automation, balance inquiries, loan status, card activations, address changes, the platform must establish authenticated API connections with enterprise cores.

Platforms without confirmed integration documentation for FIS, Fiserv, Plaid, or Symitar should be treated as unproven in your environment until integration is demonstrated, not promised.

Failure Point 4: Vague compliance marketing

Vendors claiming to be ‘fully compliant’ without specifying which standards, which audit cycle, and which scope are not making a compliance claim. They are making a marketing claim.

Required certifications for a production banking deployment include SOC 2 Type II, PCI-DSS Level 1 (for any call touching payment card data), GLBA technical safeguards compliance, and granular audit-trail logging. Require documentation, not declarations. Any vendor offering financial services AI calling compliance without documented audit controls, authentication safeguards, and retention policies should be treated cautiously during procurement

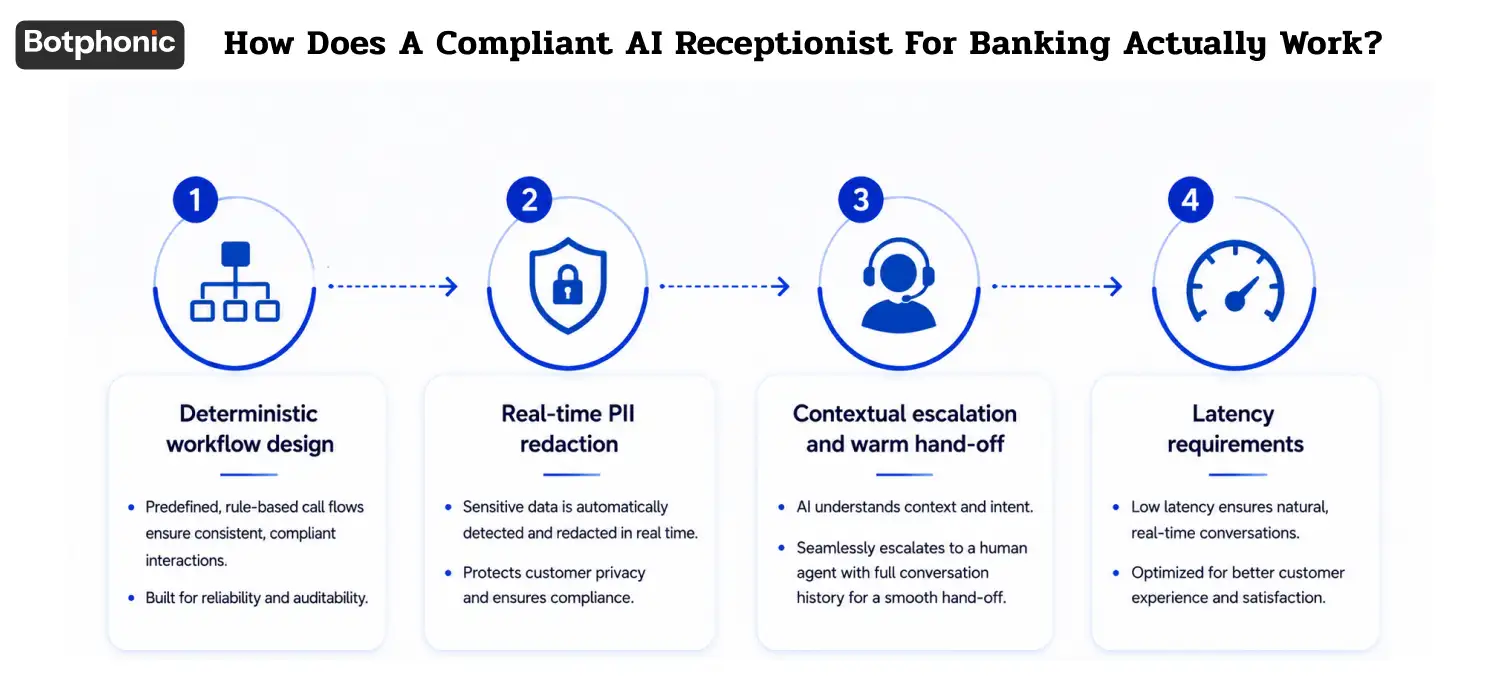

How Does a Compliant AI Receptionist for Banking Actually Work?

A compliant banking AI receptionist works by separating what the AI retrieves from what the AI generates, and enforcing strict boundaries at every layer. Here’s what that means for your architecture evaluation.

PRO TIP

PRO TIP

1. Deterministic workflow design

Deterministic pipelines route customer intents to pre-approved response nodes. The AI identifies what the customer is asking. It then retrieves the approved response for that intent, it does not write one.

This design means every response your AI delivers was reviewed by your compliance team before it went live. It also means the system cannot be prompted into saying something your institution never approved.

2. Real-time PII redaction

Before any interaction data touches a log, storage layer, or analytics pipeline, account numbers, Social Security tokens, and authentication credentials must be parsed and masked. This is not optional for GLBA compliance, it is a baseline technical safeguard requirement.

Platforms without a real-time PII redaction layer are not GLBA-compliant, regardless of what their marketing materials state.

3. Contextual escalation and warm hand-off

Not every call can or should stay in the automated channel. Escalation triggers must respond to both intent (a customer asking about fraud) and sentiment (vocal stress markers indicating distress).

The escalation must be warm, meaning the human agent receives a structured summary of the interaction before picking up. Cold transfers that require customers to repeat themselves are a primary driver of abandonment and negative satisfaction scores.

4. Latency requirements

Conversational lag above 1.2 seconds destroys perceived quality during financial interactions. Customers interpret delay as system confusion or call routing errors. Sub-300ms response latency, achievable with platforms like Botphonic, is the benchmark for high-volume banking voice automation.

Which AI Receptionist Platforms Actually Meet Financial-Grade Requirements?

Several platforms meet financial-grade requirements, but not every Financial services solution is designed for regulated conversational workflows at enterprise banking scale.

Platform comparison by use case

| Platform | Best For | Avg. Response | Key Certifications | Core Banking Integrations |

| Kore.ai BankAssist | Large retail banks, mainframe infrastructure | ~800ms | SOC 2 Type II, PCI-DSS, GDPR | FIS, Fiserv, custom enterprise APIs |

| IBM Watsonx Assistant | Deep mainframe orchestration, enterprise scale | ~700ms | SOC 2 Type II, FedRAMP, ISO 27001 | Fiserv, custom middleware |

| Posh Technologies | Credit unions, community banks | ~500ms | SOC 2 Type II, NCUA examination-ready | Symitar, CU*Answers, Corelation |

| Botphonic | High-volume lenders, loan tracking, CRM booking | <300ms | SOC 2 Type II, PCI-DSS Level 1 | Salesforce, HubSpot, open API |

| Talkdesk Financial Services Cloud | Wealth management, CCaaS ecosystem integration | ~600ms | SOC 2 Type II, PCI-DSS, GDPR | FIS, Fiserv, Salesforce FSC |

What financial institutions actually experience in production

In practice, the gap between vendor demos and production performance is widest at the core integration layer. Credit unions deploying Posh Technologies on Symitar cores consistently report faster time-to-value than larger institutions deploying general-purpose platforms, because the core integration is pre-built rather than custom-engineered.

High-volume lenders using Botphonic for loan application status calls report that sub-300ms response latency meaningfully reduces call abandonment on automated channels, particularly during peak origination periods when queue times on human agent lines exceed 8–12 minutes.

The operational lesson: match the platform to your core, not to the most impressive demo.The strongest financial services solution platforms prioritize compliance architecture, deterministic workflows, and secure automation over flashy conversational features.

Is Deploying an AI Receptionist Worth the Investment for a Bank or Credit Union?

Yes, for institutions above a threshold call volume, the cost reduction case is straightforward. Here’s what that means in real numbers.

Standard human tier-1 call handling costs between $4.00 and $6.00 per interaction when fully loaded with staffing, telephony, and quality assurance overhead. Automated transaction handling via a compliant AI platform runs under $0.50 per call at scale. For an institution handling 10,000 routine inquiries per month, that is a cost delta of $35,000–$55,000 per month.

Beyond direct cost reduction, the operational benefits compound. Peak queue wait times drop when routine calls no longer reach human agents. Fraud response time improves when the AI can immediately route flagged interactions to a priority queue. Agent burnout decreases when repetitive balance inquiries are removed from the queue.

When not to deploy AI voice automation

Three conditions make AI voice deployment inadvisable regardless of vendor quality.

- Low overall interaction volume. If your institution handles fewer than 2,000 inbound calls per month, the infrastructure cost and compliance overhead likely exceeds the labor savings.

- Fragmented legacy telephony without standard SIP trunking. Platforms cannot integrate with telephony architectures that lack SIP compatibility without expensive middleware engineering.

- No middleware API layer connecting your telephony environment to your core banking system. Without this layer, the AI cannot retrieve account data, and becomes an expensive auto-attendant.

The phased deployment approach that reduces risk

Phase 1 (Weeks 1–4): Restrict the platform to unauthenticated inquiries only. Branch locations, routing transit codes, operating hours. No authentication, no account data. This phase establishes baseline performance before any PII enters the system.

Phase 2 (Weeks 5–12): Introduce authenticated read-only access. Balance lookups, loan application status, and deposit confirmation via secure API connections to the core. This phase requires a formal compliance review before go-live.

Phase 3 (Month 4+): Activate write-access transactional capabilities, card activations, address changes, account freezes. This phase requires a full compliance audit, penetration testing of the API connection, and sign-off from your information security officer.

For a detailed checklist covering each phase, see our AI voice deployment compliance checklist for financial institutions.

See how compliant banking AI works in production.

Request a Free Demo