Summarize Content With:

“A deep-dive into PII handling, call recording consent laws, and data retention rules every agency must understand before deploying a secure AI receptionist.”

| 74%of small P&C agencies miss inbound calls | $120Kaverage annual revenue lost to unanswered calls | 12 statesrequire all-party recording consent | 8 new lawsstate privacy laws enacted in 2025 alone |

Here are the key statistics that you must know :

| Metric | Stat |

| Small P&C agencies that miss inbound calls | 74% |

| Callers who never call back after no answer | 85% |

| States requiring all-party recording consent | 12 states |

| New state privacy laws enacted in 2025 alone | 8 laws |

| Avg. annual revenue lost to unanswered calls | $120,000 |

| Insurers using AI in some capacity (2025) | 84% |

| AI compliance as top-3 vendor criterion (BCG 2026) | 73% |

Sources: Insurvoice.ai/EINPresswire 2026 | BCG AI Value Capture 2026 | Sonant AI 100+ Tools Guide 2026 | Ringover Insurance Answering Service 2026

Every unanswered call at an insurance agency is a double failure. It is money walking out the door and a potential compliance gap that regulators may one day ask about. Industry research confirms that small P&C agencies miss up to 74% of inbound calls, and 85% of callers who don’t reach an agent on the first attempt never call back moving straight to a competitor who picked up.

The business case for a secure AI receptionist for insurance agencies has never been stronger. But in a regulated industry governed by GLBA, HIPAA crossovers, state DOI rules, and a growing patchwork of all-party consent laws, “automate everything” is not a strategy it is a liability.

This guide breaks down exactly how agencies are achieving 80% call automation without a single compliance incident: what PII protections are non-negotiable, which recording consent rules apply in your state, and how long you must actually keep those AI-captured call records.

The Compliance Paradox: Why ‘Just Automate It’ Breaks in Insurance

Insurance is not like retail or hospitality. Every inbound call potentially carries protected personal information Social Security numbers, date of birth, policy numbers, vehicle VINs, medical details for health or workers’ comp lines, and even voice biometric data. The moment an AI personal assistant for insurance agents intercepts that call, your agency has created a data processing event subject to federal and state law, your E&O carrier requirements, and state Department of Insurance oversight.

“Compliance is not a feature you add to an AI receptionist after deployment. It is the foundation you build the deployment on. Agencies that treat it as an afterthought are not saving money they are creating regulatory exposure that can dwarf any efficiency gain.”

— NAIC Model Bulletin on AI Use in Insurance, 2024–2025

Non-compliance with standards like PCI-DSS alone can result in fines of $5,000 to $100,000 per month, and that is before state DOI enforcement actions or E&O premium increases enter the picture. Eight new state privacy laws were enacted in 2025 alone, each with unique requirements and cure periods ranging from 30 to 90 days.

The agencies winning at AI automation understand one fundamental principle: compliance and automation are not opposites. A well-architected secure AI receptionist for insurance agencies actually enforces compliance rules more consistently than human staff because it never forgets a consent disclosure, never skips a data field, and never stores a recording in the wrong place.

The Regulatory Stack: Every Framework Your AI Deployment Must Satisfy

Most competitors list HIPAA and call it a day. The reality for a multi-line, multi-state insurance agency is a stack of overlapping frameworks, each with distinct requirements for AI-processed data.

Regulatory Framework Matrix for Insurance AI Deployments

| Framework | Who It Covers | Key AI-Relevant Requirement | Max Penalty |

| GLBA Safeguards Rule (2023) | All insurance companies subject to FTC jurisdiction | Encryption, access controls, annual risk assessment, vendor oversight | $100K/violation |

| HIPAA | Health insurance, workers’ comp, Medicare supplement lines | PHI handling, BAA with vendors, 6-year record retention | $1.9M/year per category |

| State DOI Privacy Rules | All licensed insurance entities in each state | 8 new state laws in 2025; 30–90-day cure periods | Varies by state |

| NAIC Model AI Bulletin | All insurers in adopting states | AI governance framework, bias testing, decision auditability | Guidance only (for now) |

| FTC Act Section 5 | All businesses with AI customer interaction | No deceptive AI representations; unfair practice prohibition | Up to $51,744/violation |

| SOC 2 Type II | Required of vendors you contract | Security, availability, confidentiality + AI-specific evidence | Vendor requirement |

According to BCG’s 2026 AI Value Capture research, 73% of enterprise AI initiatives now name compliance posture as a top-three vendor selection criterion up from 41% in 2024. That number is even higher in insurance, where DOI licensing reviews can be triggered by a single consumer complaint about data mishandling.

For agencies writing health-adjacent lines Medicare supplement, supplemental health riders, workers’ compensation HIPAA crossover is the hidden risk. The moment an AI phone call assistant for insurance companies collects claim-related health information, it may be handling Protected Health Information (PHI), requiring your vendor to sign a Business Associate Agreement (BAA) before a single call is processed.

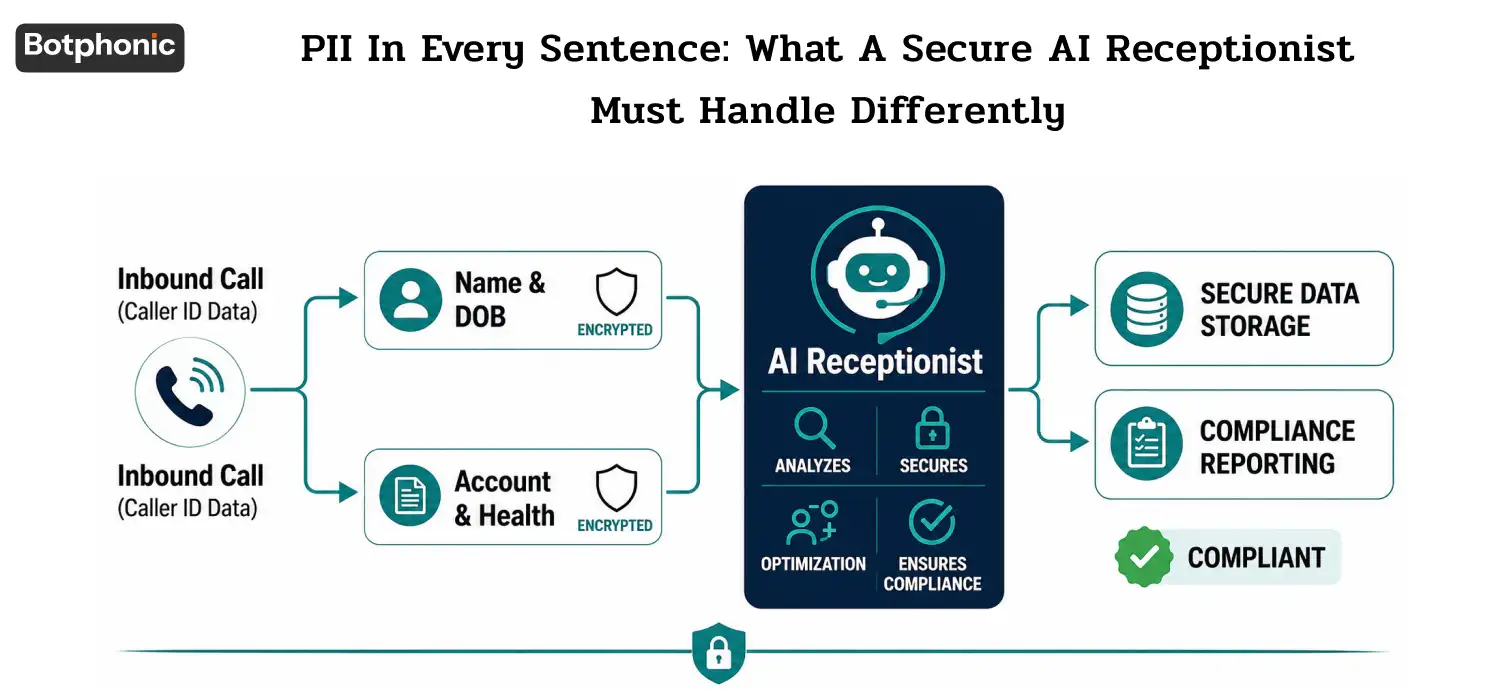

PII in Every Sentence: What a Secure AI Receptionist Must Handle Differently

Here is what most agencies do not realize: an inbound insurance call is one of the most PII-dense interactions in any industry. Within the first 60 seconds, a caller may share their full name, date of birth, policy number, vehicle VIN, property address, claims history, and health information. If your AI receptionist is not architected to handle all of that compliantly, every call is a liability event.

What counts as PII beyond the obvious

PII classification must account for indirect identifiers that become sensitive when combined vehicle VINs, policy numbers, and call metadata that individually seem benign but together identify a specific individual. Voice biometric data the unique sound signature of a caller’s voice is increasingly regulated as biometric information in states like Illinois (BIPA) and Texas, adding another layer of obligation for AI voice systems.

The shared-model training risk a question nobody asks

This is the most overlooked risk in AI vendor selection: does the platform use your customer call data to retrain its shared AI model? If the answer is yes or unclear you have a GLBA violation waiting to happen. Customer data used to train shared models creates serious regulatory risk for HIPAA and GLBA-covered entities. Make this a contractual prohibition, not just a verbal assurance.

PRO TIP

PRO TIP

Real-time PII redaction in call transcripts

Every compliant AI voice platform should automatically mask SSNs, dates of birth, account numbers, and policy identifiers during transcription — replacing them with tokens before the text is stored or transmitted. This is the difference between a transcript being a compliance asset (clean audit trail) and a compliance liability (a document full of unprotected PII sitting in a cloud database).

| Metric | Value | Source |

| Small P&C agencies missing inbound calls | 74% | Insurvoice.ai, 2026 |

| Callers who never call back after no answer | 85% | Insurvoice.ai, 2026 |

| AI compliance as top-3 vendor selection criterion | 73% of enterprises | BCG, 2026 |

| Agencies seeing productivity gains with AI | 40–60% cost reduction | Sonant AI, 2026 |

| Insurers using AI in some capacity | 84% | Sonant AI, 2026 |

| Avg. annual revenue lost to unanswered calls | $120,000 | Insurvoice.ai, 2026 |

Call Recording Consent for AI Phone Systems: The State-by-State Minefield

This is where most AI deployments fail silently not with a regulatory notice, but with a class action lawsuit. Call recording consent in the United States is a patchwork of state laws that can expose your agency to up to $1,500 per violation for AI phone agents that don’t meet 2025 consent requirements.

“The safest approach and the one most attorneys recommend is to follow the stricter standard. If there is any chance you receive calls from two-party consent states, include a recording disclosure on all calls.”

— George M. Espinoza Acosta, compliance attorney, as cited by Dialzara

One-party vs. all-party consent: the federal baseline and where it breaks

Federal wiretap law permits one-party consent meaning the party recording the conversation (your AI) counts as the consenting party. But twelve states require all-party consent for telephone calls: California, Connecticut, Florida, Illinois, Maryland, Massachusetts, Montana, Nevada, New Hampshire, Pennsylvania, Washington, and Michigan (treated as all-party by most compliance attorneys). If your caller is in any of these states, your AI must disclose recording before the call proceeds full stop.

California AB 2905 the AI-specific law that changed everything

California’s AB 2905, effective January 1, 2025, goes beyond standard consent rules it specifically targets AI interactions and imposes strict disclosure requirements, with fines of $500 per non-disclosed AI call. This means your AI receptionist or AI answering service assistant must affirmatively identify itself as artificial intelligence before the conversation begins.

Call Recording Consent Requirements by State Category (2025)

| State Category | Key States | AI Disclosure Required? | Penalty Exposure | Recommended Script |

| All-Party Consent | CA, FL, IL, PA, WA, MA, MD, NV, NH, MT | Yes (CA: mandatory AI ID) | CA: $5K/violation; PA: $1K+/day | Full pre-call consent + AI identity statement |

| One-Party Consent | TX, NY, GA, OH, AZ, CO, and most others | Best practice (not mandated) | Federal: up to $10K if misused | Recording disclosure recommended |

| Interstate Calls | Any call crossing state lines | Yes — apply strictest law | Highest applicable state penalty | Universal all-party consent script |

The universal consent script: what your AI must say first

For any agency operating across state lines, the safe approach is a universal pre-call disclosure. The AI receptionist solutions for insurance agencies should open every call with:

“Hello, you’ve reached [Agency Name]. I’m an AI assistant, and this call may be recorded for quality assurance and compliance purposes. By continuing, you consent to this recording. How can I help you today?”

That single disclosure handles all-party consent states, California’s AB 2905 AI identity requirement, and creates a timestamped consent record your audit log can reference.

Data Retention Rules for AI-Captured Insurance Calls: Keep, Protect, Delete

Data retention is the compliance issue hiding in plain sight. Most agencies think about consent and security — fewer think about how long they must keep AI-captured call data, where it must be stored, and what happens when a consumer asks for deletion.

Regulatory retention floors by framework

GLBA requires retention of certain customer financial records for a minimum of six years. HIPAA mandates six years for covered health information from the date of creation or the date it was last in effect. State DOI rules vary from three to seven years depending on the line of business. And your E&O carrier may require even longer retention periods as a condition of coverage.

The deletion conflict: privacy law vs. retention obligation

Here is the scenario nobody writes about: a policyholder in California exercises their CCPA right to deletion and asks you to erase all records of their calls. But your E&O insurer requires seven years of call documentation, and your state DOI mandates five.

The answer is a documented legal hold policy that specifies which regulatory obligation takes precedence. Typically, mandatory regulatory retention requirements override consumer deletion requests — but you must be able to demonstrate this analysis in writing.

“Security and compliance aren’t add-ons — they’re baked into everything we build. SOC 2 Type II certification gives customers third-party validation that our controls operate effectively, and HIPAA compliance ensures regulated teams can use Voice AI responsibly without slowing the business down.”

— Kevin DeMeritt, CEO, 2X Solutions

What your AI vendor contract must specify

- Explicit data retention periods for audio recordings, transcripts, and metadata — aligned to your GLBA/HIPAA obligations

- Deletion procedures and timelines with written confirmation when deletion is executed

- Data residency guarantees where physically is your call data stored? US-only processing may be required

- Breach notification SLA 72 hours or less matching GLBA prompt-notification requirements

- Prohibition on using your customer data to train any shared AI model

- Annual third-party security audit rights for your agency

The Secure AI Receptionist Vendor Audit: What Insurance Agencies Must Verify

Choosing a secure AI receptionist for insurance agencies is not a software decision — it is a compliance decision. Insurance organizations are legally responsible for compliance failures by their AI vendors, with fines up to $1.5 million per category annually for HIPAA violations, and 47% of breaches in 2025 linked to supply chain attacks.

SOC 2 Type II certification is the minimum bar. But in 2026, auditors go further: they expect AI-specific evidence including model versioning and lineage, inference logging with PII redaction policies, drift detection, and prompt-and-completion retention controls.

The subprocessor chain: where most agencies stop asking

The best AI receptionist software vendor uses a third-party large language model. Who has a BAA or data processing agreement at that layer? The compliance chain does not end at your vendor — it extends to every subprocessor that touches your caller data. Demand a full subprocessor list and confirm BAA or DPA coverage at each level before signing.

Compliant Deployment in 90 Days: A Practical Playbook

Agencies that rush deployment without a compliance architecture end up with automation that creates more problems than it solves. Here is a phased approach used by agencies that have achieved 80% call automation without a single regulatory incident.

Botphonic’s AI receptionist is built specifically for insurance agencies, with HIPAA and GLBA compliance, real-time PII redaction and automatic consent disclosures.

Book a Compliance DemoPhase 1 (Days 1–30): Compliance mapping before configuration

Identify every state your callers may be calling from. Map each call type — policy inquiry, claims intake, billing, new quote — to its automation eligibility. Document what must remain with a licensed producer. Determine your exact regulatory retention requirements across GLBA, HIPAA (if applicable), and each relevant state DOI. Only after this map is complete should you touch a configuration screen.

Phase 2 (Days 31–60): Consent architecture and PII controls

Build your universal consent script. Configure your AI to deliver it on every call, before any information is collected. Set up PII redaction rules for transcripts. Establish role-based access controls so only authorized staff can access call recordings. Have your BAA or DPA with the AI vendor signed and filed before going live.

Phase 3 (Days 61–90): Audit infrastructure and training

Document your data retention policy. Train staff on AI escalation triggers. Run your first internal compliance review of recorded calls. Set a quarterly review cadence and an annual vendor audit schedule. Financial and insurance institutions successfully deploying AI receptionists treat compliance as an ongoing process, not a one-time deployment checkbox.

Conclusion

Insurance agencies are under growing pressure to answer every inbound call while maintaining strict compliance with evolving data privacy and insurance regulations. A secure AI receptionist for insurance agencies is no longer just a productivity tool — it is becoming a critical part of operational resilience, customer retention, and regulatory protection. When implemented correctly, AI-driven call automation can reduce missed opportunities, improve response times, and create a more consistent compliance process than traditional manual workflows.

The key difference between a successful deployment and a costly compliance failure lies in preparation. Agencies must prioritize PII protection, transparent recording consent, secure data retention policies, and vendor accountability before automating customer interactions. With the right compliance-first architecture, insurance agencies can confidently automate up to 80% of inbound calls while protecting customer trust, meeting regulatory obligations, and scaling operations without increasing administrative burden.